Property Investment Mistakes: Lessons From Setbacks in My Journey

Building a property portfolio has involved good decisions, difficult periods and mistakes that changed the way I assess opportunities. The most useful lesson has not been how to avoid every setback. It has been how to recognise weak decisions, understand why they happened and turn those experiences into a more disciplined process for the next purchase.

Key Takeaway

My biggest property lessons came from overpaying, underestimating finance constraints, relying too heavily on enthusiasm and moving before the evidence was complete. Progress came from turning those experiences into a repeatable process built around clear goals, independent research, scenario testing, negotiation discipline, professional advice and honest reflection.

Before Your Next Purchase

Do not measure readiness only by whether you can obtain finance or find a property. Check whether the decision still supports your wider strategy.

1Know the purpose: Define what the property is expected to contribute to your longer-term plan.

2Test the evidence: Review the market, property, rent, condition, costs and downside risks independently.

3Protect flexibility: Consider buffers, borrowing capacity and how the purchase may affect future choices.

Why Property Mistakes Deserve an Honest Review

Property discussions often focus on successful purchases, capital growth and portfolio size. Less attention is given to the decisions that created unnecessary pressure, delayed progress or failed to perform as expected.

That can make it difficult for new investors to understand what the journey actually involves. Most long-term investors will eventually face a decision they would approach differently with the benefit of hindsight. It may be an offer made too quickly, a cost that was underestimated, a location selected on an incomplete story or a property that reduced future borrowing flexibility.

The purpose of reviewing a mistake is not to remain stuck in it. It is to identify which assumption, behaviour or process allowed the mistake to happen. Once that is clear, the experience can be converted into a practical safeguard for the future.

A lesson is only useful when it changes what you check, what you question or what you refuse to compromise on next time.

Start With a Clear Reason for Investing

When I began investing, my motivation was to build greater financial security and create more choices for my family. That purpose helped me stay committed, but I eventually learned that motivation alone is not a property strategy.

A clear reason for investing should influence the decisions that follow. Someone seeking long-term portfolio growth may assess a property differently from someone prioritising near-term cash flow, retirement planning or lifestyle flexibility. The objective does not identify the exact property to buy, but it gives you a standard against which each opportunity can be tested.

It is also important to revisit that purpose as circumstances change. Income, family responsibilities, borrowing capacity, risk tolerance and available time may all shift. A strategy that suited the beginning of the journey may need to be adjusted later.

Write the objective before reviewing properties.State what the next property is expected to do, what risks are unacceptable and what trade-offs you are prepared to make. This makes it harder to change the strategy simply because a particular listing looks exciting.

Turn the Goal Into a Practical Property Brief

A broad objective such as “build wealth through property” is difficult to use when comparing two opportunities. A practical brief turns the objective into measurable criteria and rejection rules.

The brief does not need to predict the future. Its purpose is to describe the conditions under which a property may be suitable and identify the reasons it should be rejected.

Strategy fitDefine the role the property should play and how it complements any assets already held.

Financial limitsSet a maximum purchase range, holding-cost tolerance and minimum cash reserve.

Location criteriaIdentify the demand drivers, amenities, employment access and supply risks that matter.

Property criteriaDefine suitable dwelling types, layouts, condition, land features and tenant appeal.

Risk limitsDecide which renovation, vacancy, insurance, planning or concentration risks are unacceptable.

Exit optionsConsider whether the property could appeal to more than one buyer or tenant group.

A written brief creates a reference point when a property looks attractive but does not meet the original strategy. It also helps advisers, buyers agents and finance professionals understand the decision you are trying to make.

Education Helps, but Information Is Not the Same as a Process

Early in my journey, I invested time and money in education that often focused more on possibility than execution. Courses, podcasts, seminars and investor groups can introduce useful concepts, but collecting information does not automatically improve a buying decision.

The improvement came when I began connecting education to a repeatable process: setting a brief, researching locations, comparing sales, testing rental evidence, reviewing property risks, understanding costs and deciding on a walk-away position before negotiating.

A good mentor should help you improve how you think rather than simply tell you what to buy. For investors who want structured guidance, property mentoring can provide a framework for questioning assumptions, reviewing evidence and understanding how individual purchases affect a wider portfolio.

No mentor removes the need for independent finance, legal, tax or financial advice. Their value is in helping you develop stronger questions and a more consistent decision-making process.

Learn to Separate Advice, Opinion and Sales Information

Property buyers receive information from many sources: selling agents, developers, property managers, mortgage brokers, buyers agents, accountants, building inspectors, social media groups and other investors. Each source may contribute useful information, but they do not all have the same role or incentives.

A selling agent represents the vendor. A property manager may provide rental evidence but may not be assessing the purchase as part of your complete financial position. A lender assesses lending criteria, not whether the property is the right strategic purchase. A friend’s successful experience may not translate to your income, risk tolerance or borrowing profile.

A stronger process asks three questions about any important claim:

1Who supplied the information? Understand the person’s role, expertise and commercial interest.

2What evidence supports it? Look for independent data, written reports or comparable examples.

3Who should verify it? Decide whether a qualified legal, finance, tax, building or other specialist should review the issue.

Borrowing Capacity Can Change as the Portfolio Grows

One of the harder lessons was discovering that owning more property did not mean finance would automatically become easier. As my portfolio grew, lender policies, existing debt, assessed living expenses, rental-income treatment and serviceability calculations became increasingly important.

A property may look manageable when considered by itself but still reduce flexibility across the rest of the portfolio. This is why the purchase price, loan structure, cash contribution and ongoing holding costs need to be considered together rather than as separate decisions.

Investors should also be cautious about assuming that future equity will always solve finance constraints. A property may increase in value without creating sufficient serviceability for another loan. Lending rules, household income and expenses may also change.

Before buying, investors can use property resources and calculators to explore repayment and cash-flow scenarios. These tools are useful for education and preliminary modelling, but lending decisions should be reviewed with an appropriately licensed mortgage broker or lender.

A finance approval is not the same as a complete investment assessment.Consider how the purchase could affect buffers, serviceability, future lending options and the ability to respond when circumstances change.

Understand the Difference Between Purchase Price and Total Cost

Focusing only on the advertised price can make a property appear more affordable than it is. The total commitment may include stamp duty, legal work, finance costs, inspections, immediate repairs, insurance, rates, strata charges, property management, vacancy and future maintenance.

Older properties may require more maintenance than expected. Apartments may carry special levies or future capital works. New properties may include warranties but still carry valuation, settlement or rental risks. Each property type has a different cost profile.

A useful review separates costs into three groups:

Acquisition costsPurchase-related expenses such as duty, conveyancing, inspections and loan establishment costs.

Irregular costsVacancy, major repairs, special levies, compliance work or unexpected personal circumstances.

This approach helps prevent predictable costs from being treated as emergencies later.

Test the Property Against More Than One Scenario

One of the easiest mistakes is assessing a property using a single favourable forecast. A purchase can appear comfortable when the expected rent, interest cost, occupancy and maintenance assumptions all work as planned. The real test is what happens when one or more assumptions change.

Scenario testing does not predict the future. It reveals where the decision is sensitive and helps the investor understand how much room exists before the property begins placing pressure on the household or portfolio.

1Rental scenario: What happens if the rent is lower than expected or the property is vacant between tenants?

2Interest-cost scenario: How would higher repayments affect household cash flow and the ability to hold the property?

3Repair scenario: Could you manage a major appliance, roof, plumbing or building expense without depending on rent?

4Income scenario: What would happen if household income temporarily reduced?

5Exit scenario: Would the property remain attractive to a reasonable pool of buyers if it had to be sold?

The purpose is not to create fear around every possible outcome. It is to identify whether the investment remains manageable when the central forecast does not occur exactly as expected.

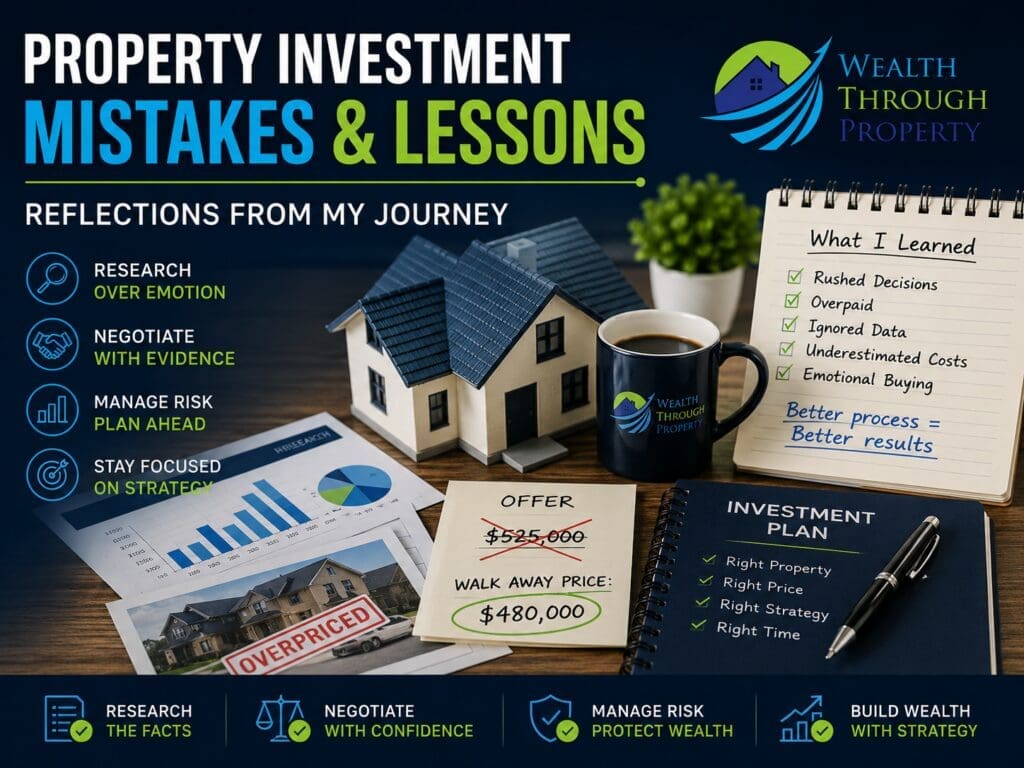

Overpaying Taught Me to Negotiate From Evidence

In my earlier purchases, I did not always negotiate with enough confidence or independent evidence. I sometimes treated securing the property as the goal instead of asking whether the final price still made sense.

Stronger negotiation begins before an offer is made. It requires an understanding of comparable sales, current competition, property condition, likely rent, vendor motivation and the terms that matter to each party. It also requires a walk-away limit set before emotion and urgency take over.

Negotiation does not always mean making the lowest possible offer. It means structuring an offer that reflects the evidence and protects the buyer from paying more than the opportunity justifies. The guide to investment property negotiation explains how comparable sales, offer terms and a walk-away position can support that process.

Missing one property may be disappointing. Overpaying for the wrong property can affect the portfolio for much longer.

Recognise the Warning Signs That Emotion Is Taking Over

Emotion is not limited to owner-occupiers. Investors can also become attached to a property, suburb, renovation idea or story about future growth. The language used during the decision often reveals when evidence is becoming secondary.

“I have already spent so much time on it.”Time spent researching a property is not a reason to proceed if the evidence no longer supports the purchase.

“Someone else will buy it.”Competition may be real, but another buyer’s urgency does not determine whether the property suits your strategy.

“It will probably grow.”A general expectation of growth should not replace an assessment of local demand, supply and property-specific risk.

“We can fix the numbers later.”Optimistic refinancing, rent or renovation assumptions should not be required to make the purchase appear viable.

“The agent said there is nothing wrong.”The selling agent represents the vendor. Independent checks remain the buyer’s responsibility.

“This is my only chance.”A clear brief helps distinguish a rare strategic fit from fear of missing out.

When several of these thoughts appear at once, it may be time to pause, revisit the brief and ask an independent person to challenge the assumptions behind the offer.

Do Not Let Momentum Replace Due Diligence

After an early purchase goes well, it can be tempting to assume the same approach will keep working. Confidence is useful, but momentum can become dangerous when it shortens the research process or makes risks feel less important.

Every property needs to earn its place in the strategy. That means reviewing the local market, buyer and tenant demand, comparable sales, property condition, planning considerations, likely maintenance, insurance, holding costs and exit options.

It also means checking whether the evidence comes from independent sources rather than relying only on the selling agent, property promoter or a single data platform. A structured data-driven due-diligence process can help separate a compelling sales story from a property supported by stronger fundamentals.

Market evidenceReview recent sales, listing conditions, rental demand and the depth of the local buyer market.

Property evidenceAssess condition, layout, maintenance exposure, restrictions and issues that may affect future use or resale.

Portfolio fitTest cash flow, risk concentration, borrowing consequences and whether the property supports the original brief.

A Five-Layer Due-Diligence Framework

Due diligence is easier to manage when the review is divided into clear layers. Each layer asks a different question and helps stop a strong feature in one area from hiding a serious weakness elsewhere.

1Strategy review: Does the property perform the role defined in the original brief?

2Market review: Are local demand, supply, employment, amenities and future development understood?

3Property review: Are the condition, layout, title, planning, strata and maintenance risks acceptable?

4Financial review: Have acquisition costs, holding costs, rent, vacancy and downside scenarios been considered?

5Professional review: Have the relevant finance, legal, building, pest, tax or specialist checks been completed?

A weak answer in one layer does not automatically mean the property should be rejected. It should trigger further investigation and a conscious decision about whether the additional risk is acceptable.

A Practical Pre-Purchase Decision Scorecard

A scorecard cannot decide whether a property should be purchased, but it can stop one exciting feature from dominating the assessment. Use the same questions for each property so opportunities are compared consistently.

1Strategy: Does the property perform the role originally defined for it?

2Location: Are demand drivers, supply conditions and local risks supported by evidence?

3Property: Does the dwelling appeal to a sufficiently broad tenant and buyer market?

4Numbers: Have rent, expenses, vacancy, maintenance and purchase costs been tested conservatively?

5Condition: Have independent building, pest, strata or specialist checks been considered where relevant?

6Finance: Is the purchase manageable without depending on the most optimistic borrowing or income assumptions?

7Negotiation: Is the offer supported by evidence, with a clear walk-away price?

8Future flexibility: Does the purchase preserve enough capacity and liquidity for likely personal and portfolio needs?

The scorecard should not be treated as a mechanical pass or fail test. Its value is in making weak assumptions visible before the buyer becomes committed to the outcome.

Prepare for Periods That Do Not Follow the Plan

Market disruptions, vacancies, repairs, changing interest costs and personal circumstances can expose weaknesses that were difficult to see when the purchase was made. The uncertainty surrounding the COVID period reinforced that a portfolio needs room for outcomes less favourable than the central forecast.

There is no single buffer amount that suits every investor. The appropriate level depends on income stability, debt, property condition, insurance, household commitments, vacancy exposure and access to liquid funds.

It can also be useful to separate foreseeable property costs from genuine emergencies. Rates, insurance, management fees and routine maintenance should form part of the expected holding budget. A separate buffer can then be available for irregular expenses, vacancy or changes in personal circumstances.

A buffer should be part of the purchase decision.It should not be whatever money happens to remain after the deposit, acquisition costs and immediate repairs have been paid.

Professional advice may be needed when assessing finance, taxation, ownership structures, insurance or personal financial risk.

Keep a Decision Journal Before You Buy

Memory changes after an outcome is known. A purchase that performs well can make the original decision appear better than it was, while an unexpected setback can make a reasonable decision appear careless. A decision journal records the thinking before the outcome is known.

Before making an offer, write down why the property fits the brief, which evidence supports the decision, the main risks, the assumptions being made and the reasons you would walk away. Also record which matters have been checked independently and which still rely on estimates.

1Investment case: Why does this property fit the strategy better than the alternatives?

2Critical assumptions: What must be true for the purchase to work as expected?

3Main risks: Which issues could create the greatest financial or practical pressure?

4Missing information: Which decisions still depend on estimates or unverified claims?

5Walk-away rules: What price, condition or new information would make you stop?

This process can reduce hindsight bias and create a clearer record for discussions with advisers and other decision-makers in the household.

Review the Decision After Settlement

Reflection should not happen only when something goes wrong. A scheduled review after settlement can identify what worked, what was missed and which parts of the process should be retained.

The review should distinguish between decision quality and outcome quality. A well-researched property can experience an unexpected event. A poorly researched property can also perform well because the market moved favourably. The outcome matters, but it does not always reveal whether the original process was sound.

1Brief review: Did the property genuinely meet the original criteria, or were the criteria changed to justify it?

2Evidence review: Which information was reliable, and which assumptions were too optimistic?

3Process review: Were inspections, professional checks and negotiations completed with enough time?

4Cost review: Which expenses were missed or underestimated?

5Change review: What specific step should be added, removed or improved before the next purchase?

Separate a Poor Decision From a Poor Outcome

This distinction has become one of the most valuable lessons in my property journey. A poor outcome does not always mean the original decision was unreasonable, and a favourable outcome does not prove the original process was strong.

A carefully researched property may experience an unexpected repair, local market change or personal event. Conversely, a property purchased with limited due diligence may rise in value because the broader market moved strongly.

Reviewing decision quality means asking whether the available evidence was considered properly at the time. This is more useful than judging the decision only by what happened afterwards.

Good processes improve the probability of better decisions. They do not remove uncertainty or guarantee a particular outcome.

Reflection Should Produce a Specific Change

It is easy to describe a purchase as a lesson without identifying what will actually be done differently. Useful reflection records what was known, what was assumed, what was missed and which part of the process needs to change.

For example, “I should have done more research” is too broad to guide the next purchase. A stronger lesson might be: “For every future property, I will manually review recent comparable sales, confirm rental evidence with more than one source and obtain written estimates for known repairs before setting my maximum offer.”

Over time, patterns may become visible—such as repeatedly underestimating maintenance, accepting optimistic rental evidence, allowing urgency to weaken negotiation discipline or failing to consider the effect of a purchase on future borrowing flexibility.

Turn every lesson into an action.Add a new question, independent check, documented limit or professional review to the process used for the next property.

Questions to Ask Before Proceeding With the Next Property

Before making the next offer, pause long enough to answer these questions in writing. The answers do not guarantee a good outcome, but they make weak assumptions easier to identify.

1Why this property? What does it contribute that the portfolio currently lacks?

2Why this location? Which demand drivers are supported by current evidence?

3Why this price? Which comparable sales and property differences support the offer?

4What could go wrong? Which risks would create the greatest financial or practical pressure?

5What remains uncertain? Which parts of the decision still rely on assumptions rather than verified information?

6What is the walk-away point? At what price or risk level does the opportunity stop supporting the strategy?

7Who has challenged the decision? Has anyone independent tested the reasoning rather than simply agreed with it?

Use Experience to Improve the Next Decision

Property investing is rarely a straight line. Some decisions will work better than expected, while others will expose gaps in research, finance planning or risk management. Neither result should be viewed in isolation.

The goal is not to build a portfolio as quickly as possible or copy another investor’s milestones. It is to make each purchase with a clearer understanding of the evidence, risks, trade-offs and effect on the wider strategy.

An investment property buyers agent may help with strategy alignment, market research, property assessment, due diligence and negotiation. That support should complement—not replace—independent financial, lending, legal, tax, building and pest advice.

Want a more structured process before your next purchase?Discuss your property goals, previous setbacks and the research process needed to approach the next opportunity with greater clarity.

What are some common mistakes made by new property investors?

Common mistakes include buying without a clear brief, relying on optimistic rental or growth assumptions, underestimating costs, skipping independent due diligence, overpaying under pressure and failing to consider how one purchase affects future borrowing flexibility.

How can investors learn from a property purchase that did not go to plan?

Review the original evidence, assumptions, advice and decision process. Identify whether the issue came from weak research, an unforeseeable event or an acceptable risk that produced an unfavourable result. Then add a specific check or control to the process used for future purchases.

What is the difference between a poor decision and a poor outcome?

A poor decision is generally based on weak evidence, ignored risks or an inconsistent process. A poor outcome can still occur after a reasonable decision because conditions change or an unexpected event occurs. Reviewing the original decision record helps separate the two.

Does making a mistake mean the entire property strategy has failed?

Not necessarily. One setback may reveal a problem with a particular property, assumption or part of the process rather than the entire strategy. The appropriate response depends on the investor’s circumstances and may require advice from qualified finance, tax, legal or property professionals.

How can an investor avoid overpaying for a property?

Review recent comparable sales, assess the property’s condition and rental evidence, understand current competition and set a walk-away limit before negotiating. No valuation method is perfect, but independent evidence provides a stronger basis than urgency or emotion.

How should an investor test whether a property remains affordable?

Consider more than the expected case. Test lower rent, vacancy, higher repayments, major repairs and temporary changes in household income. The analysis should be reviewed with appropriately qualified professionals where personal finance or lending advice is required.

How much of a financial buffer should a property investor keep?

There is no universal amount. An appropriate buffer depends on income stability, debt, household costs, property condition, vacancy risk, insurance and access to other liquid funds. Personal guidance should come from appropriately licensed professionals.

What should be included in a property decision journal?

Record the reasons for proceeding, the evidence used, the expected numbers, the main risks, the least certain assumptions, professional advice received and the conditions that would cause you to reduce the offer or walk away.

How often should an investor review their property strategy?

A strategy should be reviewed when personal circumstances, income, borrowing capacity, market conditions or long-term goals materially change. It may also be useful to review the strategy before each major purchase or refinance decision.

Can a property mentor or buyers agent prevent every investment mistake?

No adviser can remove all risk or guarantee an outcome. Good support can improve the research, questioning, property assessment and negotiation process, while specialist finance, tax, legal, building and pest advice may still be required.

```

Related support

Services and tools that connect to this topic

Move through the selected WTP pages and open the ones that connect to the article topic.